These articles discuss the real estate short sale process and how you can benefit from a the short sale process.

What Is A Short Sale and How Do I Qualify?

A short sale is a sale of real estate in [...]

These articles discuss the real estate short sale process and how you can benefit from a the short sale process.

A short sale is a sale of real estate in [...]

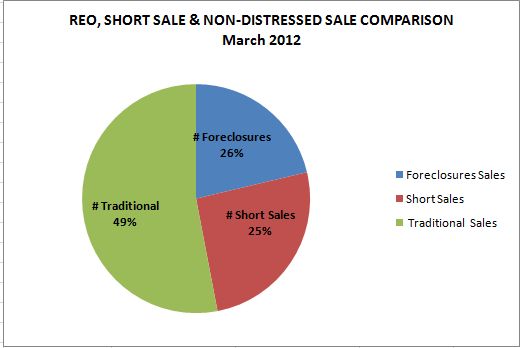

Nationwide, banks are agreeing to more short sales, and for [...]

As part of a settlement with state attorneys general, the [...]