Right now, mortgage rates are rising fast following several years of record lows. This leaves potential homebuyers wondering how they can beat the rates, and one option is buying mortgage points. With mortgage points, you can save money, but they don’t always make sense in every situation.

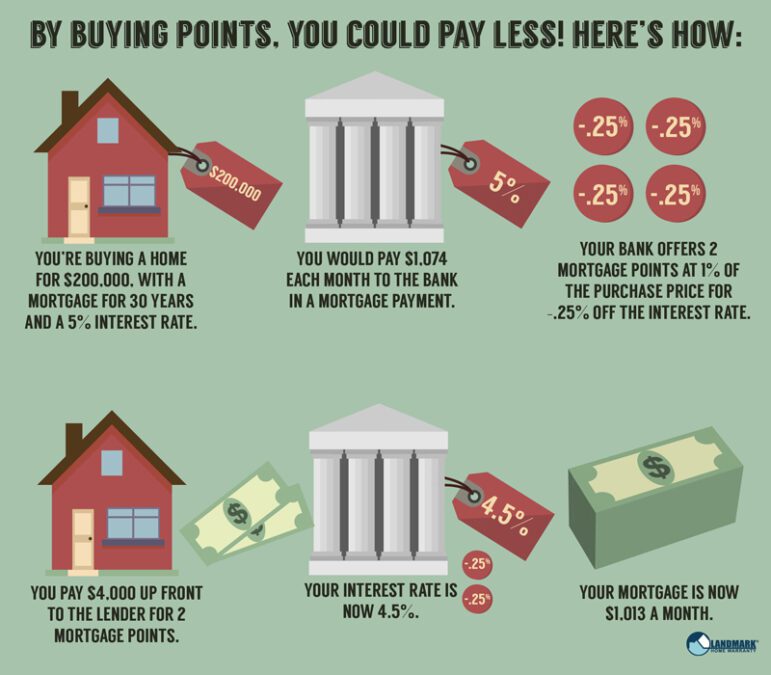

Mortgage points are a fee you, as a borrower, would pay a lender to reduce your interest rate on a home loan. You’ll hear it referred to as buying down the rate.

Each point you’re buying will cost 1% of your mortgage amount. If you’re getting a $400,000 mortgage, a point would cost $4,000.

Each point will usually lower your rate by 0.25%. One point would reduce your mortgage rate from, let’s say, 6% to 5.75% for the life of your loan.

However, there’s variation in how much every point will lower the rate. How much mortgage points can reduce your interest rate depends on the loan type and the general environment for interest rates.

You can buy more than a point, or you can buy a fraction of a point.

Your points are paid when you close, and you’ll see them listed on your loan estimate document. You receive the loan estimate document after applying for a mortgage, and you’ll also see them on your closing disclosure, which you get right before you close on your loan.

There are also mortgage origination points and fees you pay to a lender for originating, reviewing, and processing your loan. These usually cost 1% of the total mortgage.

These don’t directly reduce your interest rate. Lenders might let a borrower get a loan with no origination points, but usually, that’s in exchange for other fees or a higher interest rate.

To determine when mortgage points make sense, you have to calculate what’s known as your breakeven point. This is when borrowers can recover what they spent on prepaid interest. To calculate this, you start with what you paid for the points and divide that amount by how much money you’re saving each month with the reduced rate.

Let’s say the figure you get when calculating your breakeven point is 60 months. That means you would need to stay in your home for 60 months to recover what you spent on discount points.

If you’re buying a home you plan to stay in for a long time, then the additional costs of mortgage points to lower your interest rate can make financial sense.

If you doubt you’ll stay in your home for the long term, it’s probably not right for you.

If you don’t stay in the home for long enough, you will ultimately lose money.

At the same time, as you consider whether or not mortgage points are right for you, you should consider your down payment. You could be better off putting money towards a more significant down payment than points. If you make a larger down payment, you might be able to secure a lower interest rate. Plus, if you make a down payment of at least 20%, you can avoid the added cost of PMI.

Bigger down payments mean you’re lowering your loan-to-value ratio or the size of your mortgage in comparison to the value of your home.

The takeaway is not to assume that buying mortgage points is always the right option. You need to consider how long you will stay in the home and your breakeven point.

Seller Concessions:

In today’s market, sellers are offer large concessions to get their properties sold and as your realtor, we can help you lower your interest rate by having the seller pay for all or a portion of the rate buy-down. Give us a call today to find out how you can save thousands over the life of your loan.

Position Realty

Office: 480-213-5251