5 Critical Questions For New Real Estate Investors

There several ways to invest in real estate with single [...]

There several ways to invest in real estate with single [...]

We all work hard at our J.O.B., don’t we? We [...]

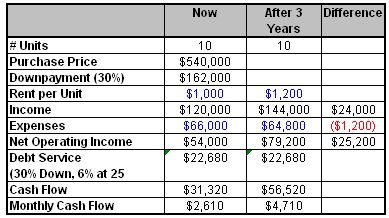

Want to increase your real estate investing properties cash flow? [...]

Many of 4-family properties sell at a price where the [...]