How To Begin Investing In Rental Properties ~ Buy and Hold

In my judgment, investing in real estate to hold is [...]

In my judgment, investing in real estate to hold is [...]

We all work hard at our J.O.B., don’t we? We [...]

More investors are rehabilitating homes and looking to sell them [...]

Here's the big question that confuses many: Can you have [...]

A 1031 exchange is a tax-deferred exchange which allows an [...]

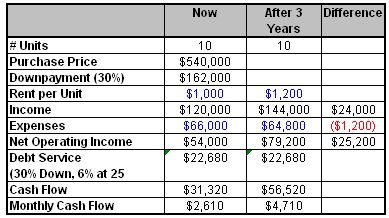

Many of 4-family properties sell at a price where the [...]