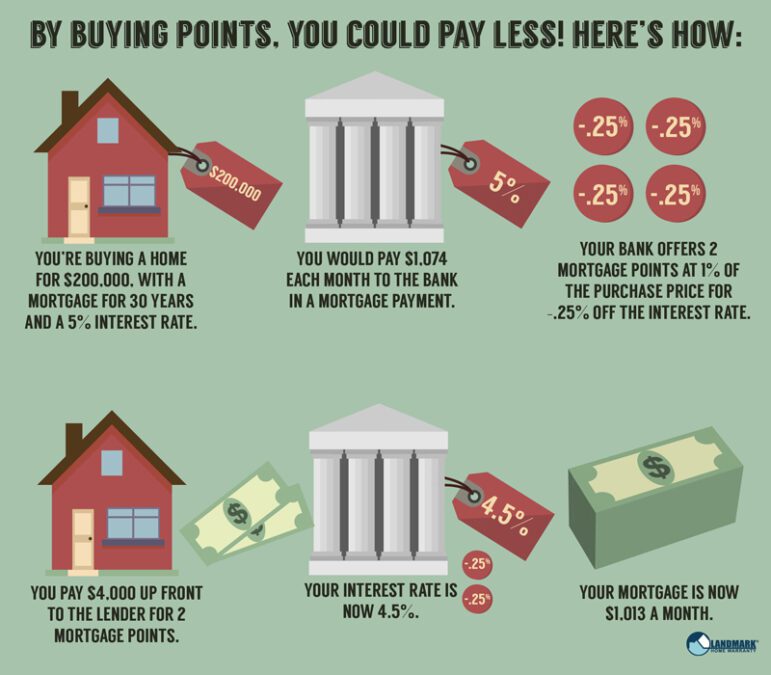

When Do Mortgage Points Make Sense?

Right now, mortgage rates are rising fast following several years [...]

Right now, mortgage rates are rising fast following several years [...]

Credit scores are simply a numerical reflection of your current [...]

A down payment is something you’re likely going to need [...]