These articles provide advice about how commercial real estate works and how to avoid making costly mistakes.

Investing In Commercial Real Estate Isn’t That Difficult

Most real estate investors start off investing in single family [...]

These articles provide advice about how commercial real estate works and how to avoid making costly mistakes.

Most real estate investors start off investing in single family [...]

In this articles, we will examine how one can use [...]

These 10 rules might seem elementary at first glance, but [...]

We all work hard at our J.O.B., don’t we? We [...]

Most real estate investors get started buying single-family houses, probably [...]

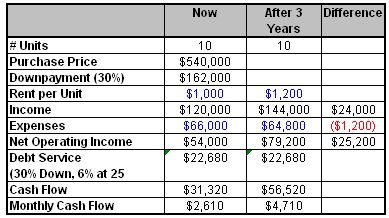

Apartment properties are preferred by many investors as they bring [...]

I was asked the other day by a new investor [...]

The quickest way I know to make significant profits with [...]

After location, zoning is probably the most important characteristic of [...]

Are commercial fixer-uppers worth the time, expense and effort? My [...]