How Does A Cloud On Title Affect Getting A Mortgage

This might be a rather obscure term for the [...]

This might be a rather obscure term for the [...]

Right now, mortgage rates are rising fast following several years [...]

Credit scores are simply a numerical reflection of your current [...]

A down payment is something you’re likely going to need [...]

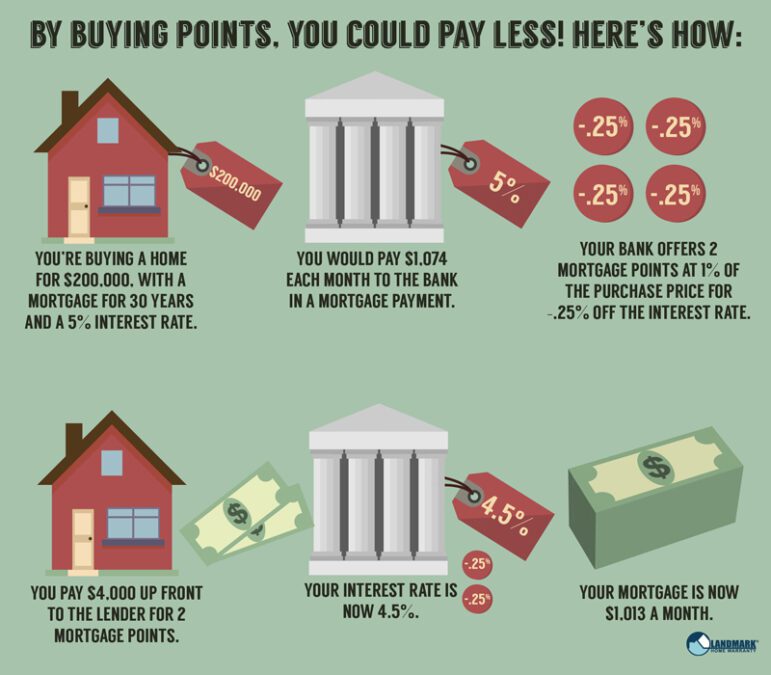

If you watch real estate shows, you might occasionally hear [...]

If you’ve ever considered buying a second home, the mortgage [...]

FHA loans are a popular choice for a lot of [...]

It is not exactly surprising, given the stunning jumps in [...]

It’s normal to romanticize buying a house. It’s one of [...]

Unfortunately, overpaying for a house is a common issue among [...]