How Donald Trump’s Policies Could Affect Phoenix Homeowners

Billionaire Donald Trump made much of his fortune as a [...]

Billionaire Donald Trump made much of his fortune as a [...]

You can't expect to reduce your risk of getting sued [...]

Your real estate professional is probably advising you to declutter, [...]

We all work hard at our J.O.B., don’t we? We [...]

One of the biggest mistakes new and veteran real estate [...]

Phoenix Home buyers who are looking for big discounts on [...]

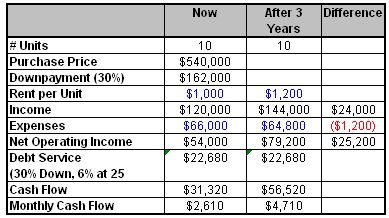

Phoenix multifamily properties are preferred by many investors as they [...]

The true goal of every investor should be to create [...]

Warren Buffett, the billionaire investor and Berkshire Hathaway CEO, said [...]

The real estate market in Phoenix, Arizona has become very [...]